Européennes

Business Cycles in Europe since 1970

This column reports the nature and the amplitude of economic cycles in the Euro area since 1970, with a focus on the role of financial factors in generating these cycles.

By Stéphane Lhuissier

In 2004, Ben Bernanke, former Chairman of the Federal Reserve, reminded the numerous benefits of a reduced macroeconomic volatility [1]:

“Lower volatility of inflation improves market functioning, makes economic planning easier, and reduces the resources devoted to hedging inflation risks. Lower volatility of output tends to imply more stable employment and a reduction in the extent of economic uncertainty confronting households and firms. The reduction in the volatility of output is also closely associated with the fact that recessions have become less frequent and less severe.”

Only a few years ago, these benefits were often taken for granted and the study of business cycle fluctuations seemed to be largely irrelevant, due to a large decline in the volatility of aggregate output in the long run, thus suggesting the definitive demise of cycles. Recent events have, however, provided evidence that the cycle is still alive. The economic consequences of the financial crisis in 2008 have recently led to revitalize the interest of the study of business cycles, in particular the role of financial markets in generating cycles, which has been so far largely underestimated by the profession.

However, most empirical works have so far exclusively focused on the United States [2], to the detriment of European business cycles. A recent CEPII Working Paper [3] fills part of this gap, by examining the amplitude and the nature of European business cycles from 1970 to today, and by drawing implications for future monetary policy.

Evidence of changes in volatility

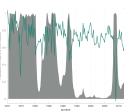

As a first step, the paper documents the strong evidence of changes in the amplitude of business cycles over time, by making a distinction between low- and high-volatility regimes [4]. Figure 1 shows that the volatility of output has changed over time, switching between the two regimes. However, it has been moderated since the beginning of the 1990s. The United States has also experienced this downward trend in output volatility, but much earlier, i.e. in the early 1980s. Finally, this trend toward greater economic stability has been temporary halted during the Great Recession in 2008.

This downward trend was not specific to output volatility and applies to a wide range of macroeconomic variables (growth rate of consumption, growth rate of wages, inflation, and short-term nominal interest rate), as shown in Figure 2. However, change in volatility does not occur simultaneously across time series. Whereas the decline in the volatility of wages and nominal interest rate coincides with that of output, inflation has moderated well before this date.

Sources of these changes

What explain these changes? The working paper shows that the decline in macroeconomic volatility beginning in the early 1990s was the result of smaller shocks hitting the economy, which were primarily associated with an improvement in productivity, as well as a better resource allocation between savers and investors [5].

The 1970s and 1980s have seen dramatic adverse technological shocks. These shocks, meaning a decrease in the pace of growth in productivity, lead to a slowdown in economic activity. The 1990s have been however, characterized by shocks that were smaller than those previously experienced, and thus contributing to the decline in output volatility.

As mentioned above, the relationships between savers and investors have been playing a crucial role in explaining economic cycles, and not only during the Great Recession. This is proved by Figure 3 that highlights the importance of “financial shocks”, defined more precisely as perturbations that directly affect the efficiency of system of financial intermediation to transform household saving into productive capital. The green solid line displays the historical path of output growth if the economy would have been hit only by these financial shocks. The grey solid line displays the actual growth rate.

This figure shows that there are important similarities between the simulated series and the actual series, suggesting that these shocks have been playing a crucial role in generating the fluctuations of the output growth, especially since the launch of the euro in 1999. In particular, financial intermediaries have fostered the pace of economic activity during the early 2000s. Efficient financial intermediation implied a reduction of the cost of transferring funds from savers to investors, who ultimately convert them into productive capital. Not surprisingly, the output collapse after the financial crisis results from a sudden and long-lasting tightening of credit conditions. These results that attribute the rise and the fall of economic activity to financial factors is a clear illustration of what the former British Prime Minister, William Gladstone, said in 1858: “Finance is, at it were, the stomach of the country, from which all the other organs take their tone.”

What are the implications for monetary policy?

The European Central Bank (ECB) Statute clearly states that the primary objective of monetary policy is to maintain price stability.

Therefore, if financial shocks affect permanently and systematically macroeconomic fluctuations, ECB should integrate financial stability in its mandate. The key question is, of course, how it should be done. Olivier Blanchard advocates the development of new macroprudential tools in order to set up defenses against the “procyclicality” of financial markets that permanently amplify business cycles, and to strengthen the capacity of financial sector to absorb adverse financial shocks. This will enable monetary policy to “focus on its usual business –inflation targeting”. Economists are far from unanimous about such a proposal. Michael Woodford, a Columbia University Professor, suggests to shift from inflation targeting to nominal income targeting, with no particular focus on financial stability. From a totally different angle, research economists at the Federal Reserve of New York highlights the need to take into account the level of risk taking in financial markets when conducting monetary policy [6].

References

Olivier Blanchard & John Simon, 2001. "The Long and Large Decline in U.S. Output Volatility," Brookings Papers on Economic Activity, Economic Studies Program, The Brookings Institution, vol. 32(1), pages 135-174.

Jonas D. M. Fisher, 2006. "The Dynamic Effects of Neutral and Investment-Specific Technology Shocks," Journal of Political Economy, University of Chicago Press, vol. 114(3), pages 413-451, June.

Alejandro Justiniano & Giorgio E. Primiceri, 2008. "The Time-Varying Volatility of Macroeconomic Fluctuations," American Economic Review, American Economic Association, vol. 98(3), pages 604-41, June.

James H. Stock & Mark W. Watson, 2003. "Macroeconomic Forecasting Using Diffusion Indexes," Journal of Business & Economic Statistics, American Statistical Association, vol. 20(2), pages 147-62, April.

James H. Stock & Mark W. Watson, 2003. "Has the business cycle changed?," Proceedings - Economic Policy Symposium - Jackson Hole, Federal Reserve Bank of Kansas City, pages 9-56.

Stéphane Lhuissier, 2015. "The Regime-switching Volatility of Euro Area Business Cycles," CEPII Working Paper.

Zheng Liu & Daniel F. Waggoner & Tao Zha, 2011. "Sources of macroeconomic fluctuations: A regime?switching DSGE approach," Quantitative Economics, Econometric Society, vol. 2(2), pages 251-301, 07.

“Lower volatility of inflation improves market functioning, makes economic planning easier, and reduces the resources devoted to hedging inflation risks. Lower volatility of output tends to imply more stable employment and a reduction in the extent of economic uncertainty confronting households and firms. The reduction in the volatility of output is also closely associated with the fact that recessions have become less frequent and less severe.”

Only a few years ago, these benefits were often taken for granted and the study of business cycle fluctuations seemed to be largely irrelevant, due to a large decline in the volatility of aggregate output in the long run, thus suggesting the definitive demise of cycles. Recent events have, however, provided evidence that the cycle is still alive. The economic consequences of the financial crisis in 2008 have recently led to revitalize the interest of the study of business cycles, in particular the role of financial markets in generating cycles, which has been so far largely underestimated by the profession.

However, most empirical works have so far exclusively focused on the United States [2], to the detriment of European business cycles. A recent CEPII Working Paper [3] fills part of this gap, by examining the amplitude and the nature of European business cycles from 1970 to today, and by drawing implications for future monetary policy.

Evidence of changes in volatility

As a first step, the paper documents the strong evidence of changes in the amplitude of business cycles over time, by making a distinction between low- and high-volatility regimes [4]. Figure 1 shows that the volatility of output has changed over time, switching between the two regimes. However, it has been moderated since the beginning of the 1990s. The United States has also experienced this downward trend in output volatility, but much earlier, i.e. in the early 1980s. Finally, this trend toward greater economic stability has been temporary halted during the Great Recession in 2008.

|

Figure 1: volatility of European GDP growth rate

|

|

|

Note : This figure shows the output growth rate from 1970 to 2012 (green solid line), in tandem with the probability of this indicator to be in a high-volatility regime (grey areas). The quarterly output growth rate is draws from the AWM database.

|

This downward trend was not specific to output volatility and applies to a wide range of macroeconomic variables (growth rate of consumption, growth rate of wages, inflation, and short-term nominal interest rate), as shown in Figure 2. However, change in volatility does not occur simultaneously across time series. Whereas the decline in the volatility of wages and nominal interest rate coincides with that of output, inflation has moderated well before this date.

|

Figure 2: growth rate of consumption, growth rate of wages, inflation, and short-term nominal interest rate

|

|

|

Note : This figure shows the probability of being in the high-volatility regime from 1970 to 2012 for four macroeconomic indicators: consumption, wages, inflation and Euribor three-month.

|

Sources of these changes

What explain these changes? The working paper shows that the decline in macroeconomic volatility beginning in the early 1990s was the result of smaller shocks hitting the economy, which were primarily associated with an improvement in productivity, as well as a better resource allocation between savers and investors [5].

The 1970s and 1980s have seen dramatic adverse technological shocks. These shocks, meaning a decrease in the pace of growth in productivity, lead to a slowdown in economic activity. The 1990s have been however, characterized by shocks that were smaller than those previously experienced, and thus contributing to the decline in output volatility.

As mentioned above, the relationships between savers and investors have been playing a crucial role in explaining economic cycles, and not only during the Great Recession. This is proved by Figure 3 that highlights the importance of “financial shocks”, defined more precisely as perturbations that directly affect the efficiency of system of financial intermediation to transform household saving into productive capital. The green solid line displays the historical path of output growth if the economy would have been hit only by these financial shocks. The grey solid line displays the actual growth rate.

|

Figure 3: importance of “financial shocks” in business cycles

|

|

|

|

This figure shows that there are important similarities between the simulated series and the actual series, suggesting that these shocks have been playing a crucial role in generating the fluctuations of the output growth, especially since the launch of the euro in 1999. In particular, financial intermediaries have fostered the pace of economic activity during the early 2000s. Efficient financial intermediation implied a reduction of the cost of transferring funds from savers to investors, who ultimately convert them into productive capital. Not surprisingly, the output collapse after the financial crisis results from a sudden and long-lasting tightening of credit conditions. These results that attribute the rise and the fall of economic activity to financial factors is a clear illustration of what the former British Prime Minister, William Gladstone, said in 1858: “Finance is, at it were, the stomach of the country, from which all the other organs take their tone.”

What are the implications for monetary policy?

The European Central Bank (ECB) Statute clearly states that the primary objective of monetary policy is to maintain price stability.

Therefore, if financial shocks affect permanently and systematically macroeconomic fluctuations, ECB should integrate financial stability in its mandate. The key question is, of course, how it should be done. Olivier Blanchard advocates the development of new macroprudential tools in order to set up defenses against the “procyclicality” of financial markets that permanently amplify business cycles, and to strengthen the capacity of financial sector to absorb adverse financial shocks. This will enable monetary policy to “focus on its usual business –inflation targeting”. Economists are far from unanimous about such a proposal. Michael Woodford, a Columbia University Professor, suggests to shift from inflation targeting to nominal income targeting, with no particular focus on financial stability. From a totally different angle, research economists at the Federal Reserve of New York highlights the need to take into account the level of risk taking in financial markets when conducting monetary policy [6].

References

Olivier Blanchard & John Simon, 2001. "The Long and Large Decline in U.S. Output Volatility," Brookings Papers on Economic Activity, Economic Studies Program, The Brookings Institution, vol. 32(1), pages 135-174.

Jonas D. M. Fisher, 2006. "The Dynamic Effects of Neutral and Investment-Specific Technology Shocks," Journal of Political Economy, University of Chicago Press, vol. 114(3), pages 413-451, June.

Alejandro Justiniano & Giorgio E. Primiceri, 2008. "The Time-Varying Volatility of Macroeconomic Fluctuations," American Economic Review, American Economic Association, vol. 98(3), pages 604-41, June.

James H. Stock & Mark W. Watson, 2003. "Macroeconomic Forecasting Using Diffusion Indexes," Journal of Business & Economic Statistics, American Statistical Association, vol. 20(2), pages 147-62, April.

James H. Stock & Mark W. Watson, 2003. "Has the business cycle changed?," Proceedings - Economic Policy Symposium - Jackson Hole, Federal Reserve Bank of Kansas City, pages 9-56.

Stéphane Lhuissier, 2015. "The Regime-switching Volatility of Euro Area Business Cycles," CEPII Working Paper.

Zheng Liu & Daniel F. Waggoner & Tao Zha, 2011. "Sources of macroeconomic fluctuations: A regime?switching DSGE approach," Quantitative Economics, Econometric Society, vol. 2(2), pages 251-301, 07.

[1] See “Back to the Great Moderation?”, by Stéphane Lhuissier, on Le blog du CEPII, April 30, 2015 for further discussion.

[2] Many studies have now well-documented and attempted to understand the persistent and large variations in growth rates of U.S. real GDP since the post World War II [Among others, Kim and Nelson (1998), Blanchard and Simon (2001), Stock and Watson (2002,2003), Fisher (2006), Justiniano and Primiceri (2008) and Liu, Waggoner and Zha (2011)]. Although all economists agree that U.S. macroeconomic volatility declined in the mid 1980s, different views exist regarding the source of this change. There are three main explanations, namely structural changes, good luck (shocks have been smaller and less frequent), and improved macroeconomic policies.

[4] The amplitude of business cycles is usually measured by the level of volatility in the growth rate of a macroeconomic time series. To capture changes in the volatility over time, the paper is based upon the assumption that the economy can switch between two volatility regimes, which are quantitatively and qualitatively different. Such a framework allows for identifying variations in the sources of economic disturbances over time.

[5] These two main sources have been identified through a Dynamic Stochastic General Equilibrium (DSGE) in which shock variances can change over time.

< Back