Six pack: the case for a simplified scoreboard

In December 2011, the ‘six pack’ introduced a new surveillance procedure of macroeconomic imbalances at the European level. However, the ten indicators used for the early warning of imbalances do not seem much more relevant than the simple indicator of the current account balance.

By Laurence Nayman, Sophie Piton, Agnès Bénassy-Quéré

The euro-zone crisis is not only about public finances. Up to 2007, Spain and Ireland did not breach the Stability and Growth Pact (SGP). In both countries, it was private (banking or mortgages) and not public indebtedness that was at the heart of the economic tensions.

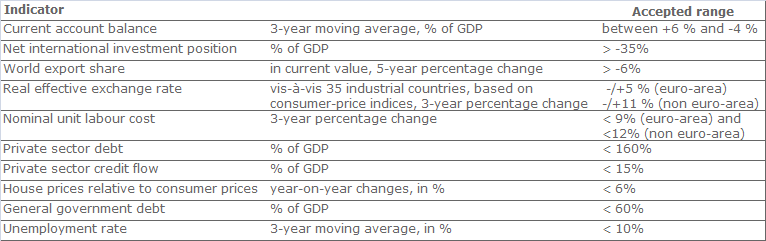

From the beginning of the crisis, Europeans became aware of the excessive importance given to the surveillance of member states’ public finances [1]. Beyond a reinforced fiscal surveillance, the six pack (a legislative package of five regulations and one directive entered into force in December 2011), introduces a new surveillance mechanism for the prevention and correction of macroeconomic imbalances. This Macroeconomic Imbalance Procedure (MIP) is composed of both a preventive arm (with an alert mechanism) and a corrective arm (with sanctions in case of an excessive imbalance). The alert mechanism consists of an economic reading of a scoreboard composed of ten early warning indicators (see table 1) from which countries at risk are identified. The European Commission then runs an in-depth analysis to determine whether the imbalances revealed by the indicators are worrying.

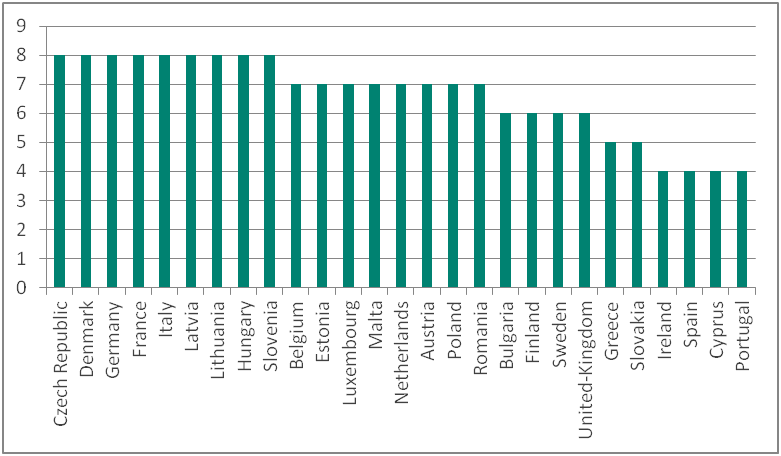

In February 2012, the European Commission published on its website the performance of member states regarding the scoreboard and its ten indicators. Results are synthesized in figure 1.

In May, twelve in-depth analyses were run for Belgium, Bulgaria, Cyprus, Denmark, Finland, France, Italy, Hungary, Slovenia, Spain, Sweden and the United-Kingdom. Excluding the three “programme-countries” – Greece, Ireland and Portugal – can easily be understood since these are already closely monitored by the Troïka. However, the choice of the twelve countries does not mirror the “grades” resulting from the scoreboard. Thus, one can question the relevance of such scoreboard regarding its objective: an early warning of member states’ macroeconomic imbalances.

Some indicators seem hardly appropriate. For example, the real effective exchange rate is computed against a basket of 35 industrial countries, and so, is by definition, mainly influenced by the euro’s real exchange rate. Export market shares growth mirrors the weight of Europe in world trade or the integration of the country in the value added chain rather than a trend of the export performance. Thus, in 2010, in relation with the global crisis, even Germany didn’t abide by the threshold set by the Commission. Furthermore, some other indicators, like private sector credit flows or private and public indebtedness, are already accounted in the current account balance.

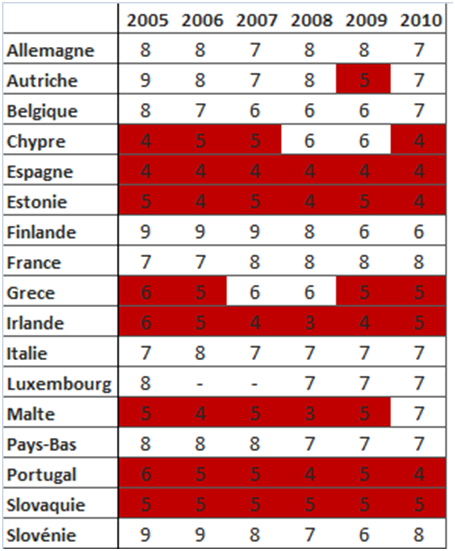

Looking backwards, would the scoreboard have been able to point at countries that have experienced a harsh crisis since 2008? As shown in table 2, between 2005 and 2008 no country fills all the requirements of the scoreboard. By the yardstick of a mark below the average of the euro zone –namely 7/10 in 2005, then 6/10 the following years – Spain, Ireland and Portugal clearly left the track with scores between 3 and 6/10, but Cyprus and Greece filled the criteria on average for two years. Besides, the scoreboard provides early warning for Malta, Estonia and Slovakia, three countries that were not directly hit by the crisis.

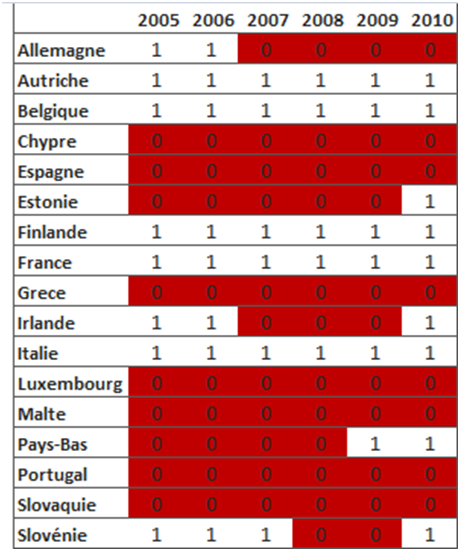

How would a criterion of current account balance alone have performed? Between 2005 and 2008, all the countries currently affected by the crisis (except Italy) did exceed the 4% threshold for the current account deficit, Ireland following suit in 2007. This sole indicator rings the bell hardly more often than the complete scoreboard. This metrics based on current transactions is easy to compute and to some extent, synthesises the macroeconomic imbalances of a country. Besides, Frankel and Saravelos [2] have shown its relevance to forewarn economic crises. However, it is not sufficient per se, some deficits being potentially ‘good’ deficits. But the scoreboard is not designed either to be self-reliant: it only serves as an alert mechanism; it also accounts for an in-depth analysis that will typify each situation and will determine the nature and magnitude of the imbalances.

Table 1 – Scoreboard for the surveillance of macroeconomic imbalances

Source: European Commission (2012) “Scoreboard for the surveillance of macroeconomic imbalances”, Occasional Paper 92, February.

Source: European Commission (2012) “Scoreboard for the surveillance of macroeconomic imbalances”, Occasional Paper 92, February.

Figure 1 – Countries’ ‘grades’ regarding the scoreboard in 2012*

* Number of satisfied criteria over 10.

Source: European Commission, February 2012.

Table 2 – Countries’ ‘grades’ depending on two alternative criteria, 2005 to 2010

Note: If the country fills one criterion we attribute it 1 point, otherwise 0 point. The grade over 10 corresponds to the number of indicators the country fills out of ten indicators. The red cells correspond to a performance under the average of the Euro zone (Table 2 (a)) or to a current account balance >+6% / <-4% (Table 2 (b)).

Source: Eurostat, CEPII.

From the beginning of the crisis, Europeans became aware of the excessive importance given to the surveillance of member states’ public finances [1]. Beyond a reinforced fiscal surveillance, the six pack (a legislative package of five regulations and one directive entered into force in December 2011), introduces a new surveillance mechanism for the prevention and correction of macroeconomic imbalances. This Macroeconomic Imbalance Procedure (MIP) is composed of both a preventive arm (with an alert mechanism) and a corrective arm (with sanctions in case of an excessive imbalance). The alert mechanism consists of an economic reading of a scoreboard composed of ten early warning indicators (see table 1) from which countries at risk are identified. The European Commission then runs an in-depth analysis to determine whether the imbalances revealed by the indicators are worrying.

In February 2012, the European Commission published on its website the performance of member states regarding the scoreboard and its ten indicators. Results are synthesized in figure 1.

In May, twelve in-depth analyses were run for Belgium, Bulgaria, Cyprus, Denmark, Finland, France, Italy, Hungary, Slovenia, Spain, Sweden and the United-Kingdom. Excluding the three “programme-countries” – Greece, Ireland and Portugal – can easily be understood since these are already closely monitored by the Troïka. However, the choice of the twelve countries does not mirror the “grades” resulting from the scoreboard. Thus, one can question the relevance of such scoreboard regarding its objective: an early warning of member states’ macroeconomic imbalances.

Some indicators seem hardly appropriate. For example, the real effective exchange rate is computed against a basket of 35 industrial countries, and so, is by definition, mainly influenced by the euro’s real exchange rate. Export market shares growth mirrors the weight of Europe in world trade or the integration of the country in the value added chain rather than a trend of the export performance. Thus, in 2010, in relation with the global crisis, even Germany didn’t abide by the threshold set by the Commission. Furthermore, some other indicators, like private sector credit flows or private and public indebtedness, are already accounted in the current account balance.

Looking backwards, would the scoreboard have been able to point at countries that have experienced a harsh crisis since 2008? As shown in table 2, between 2005 and 2008 no country fills all the requirements of the scoreboard. By the yardstick of a mark below the average of the euro zone –namely 7/10 in 2005, then 6/10 the following years – Spain, Ireland and Portugal clearly left the track with scores between 3 and 6/10, but Cyprus and Greece filled the criteria on average for two years. Besides, the scoreboard provides early warning for Malta, Estonia and Slovakia, three countries that were not directly hit by the crisis.

How would a criterion of current account balance alone have performed? Between 2005 and 2008, all the countries currently affected by the crisis (except Italy) did exceed the 4% threshold for the current account deficit, Ireland following suit in 2007. This sole indicator rings the bell hardly more often than the complete scoreboard. This metrics based on current transactions is easy to compute and to some extent, synthesises the macroeconomic imbalances of a country. Besides, Frankel and Saravelos [2] have shown its relevance to forewarn economic crises. However, it is not sufficient per se, some deficits being potentially ‘good’ deficits. But the scoreboard is not designed either to be self-reliant: it only serves as an alert mechanism; it also accounts for an in-depth analysis that will typify each situation and will determine the nature and magnitude of the imbalances.

Table 1 – Scoreboard for the surveillance of macroeconomic imbalances

Figure 1 – Countries’ ‘grades’ regarding the scoreboard in 2012*

* Number of satisfied criteria over 10.

Source: European Commission, February 2012.

Table 2 – Countries’ ‘grades’ depending on two alternative criteria, 2005 to 2010

(a) regarding the scoreboard (over 10) |

(b) regarding the current account balance (over 1) |

Source: Eurostat, CEPII.

[1] The necessity to expand the surveillance to all saving-investment imbalances was already pointed out in 2003 by CEPII. See A. Bénassy-Quéré, «The stability pact: two objectives, two rules », La Lettre du CEPII n°224, June 2003.

[2] Frankel, Jeffrey and George Saravelos (2010), “Are Leading Indicators of Financial Crises Useful for Assessing Country Vulnerability? Evidence from the 2008-09 Global Crisis,” NBER Working Paper 16047, June.

< Back